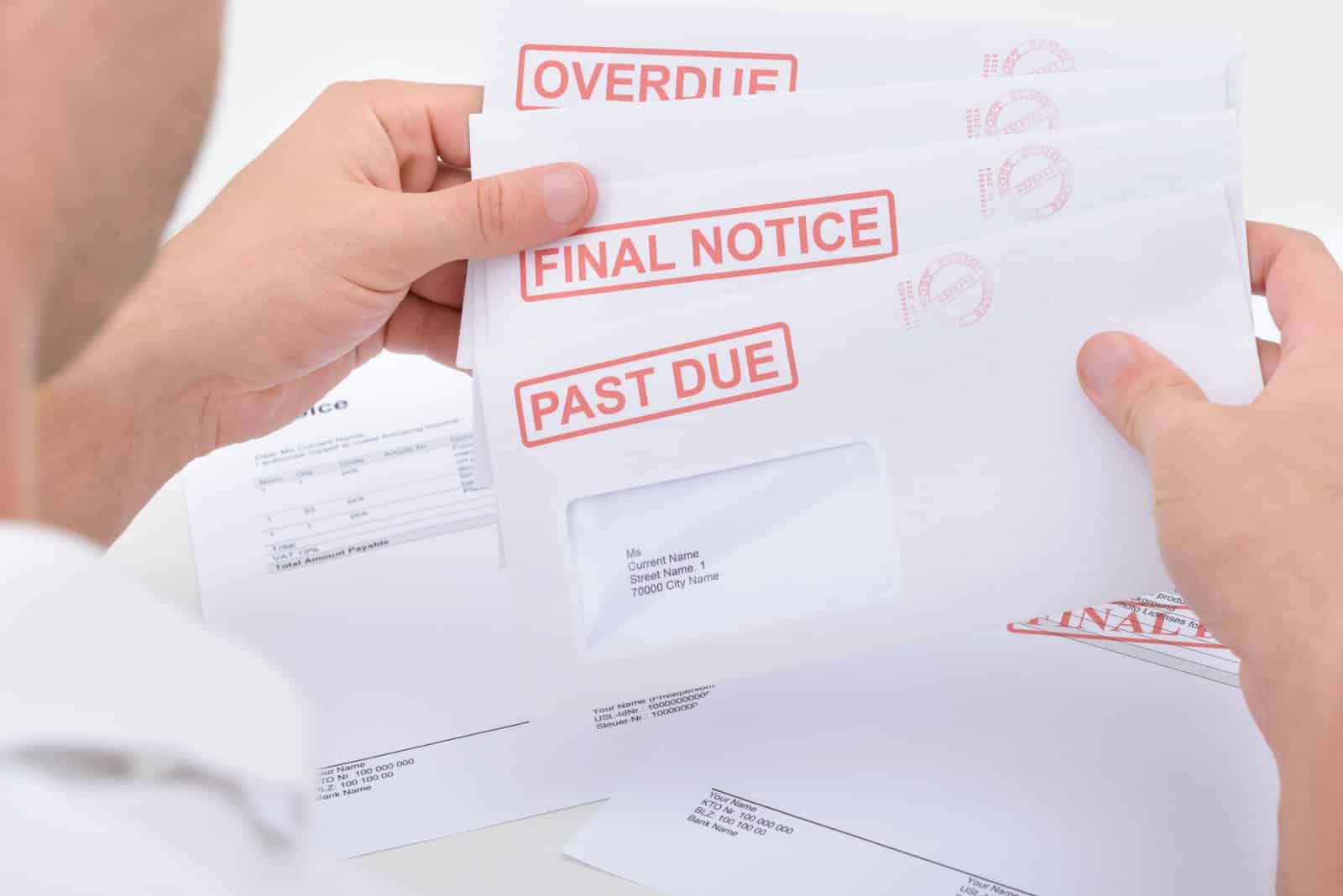

The Biden administration is taking steps to put a cap on how much banks can charge consumers for being late on credit card payments. This proposal is causing quite the stir among banks and credit card companies. While the plan could save people billions, industry experts are concerned it might end up causing more problems than it solves.

A Bold Initiative

The Consumer Financial Protection Bureau (CFPB) is leading the charge against what they see as unfair charges by big credit card companies.

CFPB head Rohit Chopra wants to slash late fees to $8, saying it is necessary to stop credit card companies from making a fortune off customers for trivial errors and oversights.

Industry Backlash

Not everyone is on board with this idea. Figures like Rob Nichols, head of the American Bankers Association, are critical, arguing that the new rule could encourage more late payments and negatively impact people’s credit scores.

Concerns Over Consumer Impact

The banking sector warns that capping late fees could force them to tighten lending criteria and increase interest rates for everyone, not just those who pay late. This could mean even diligent payers might feel the pinch.

The Credit Line Conundrum

Financial experts worry that capping fees at a level below the actual costs incurred by banks could force issuers to reassess their lending practices. This may result in stricter standards for new accounts, affecting consumers’ access to credit.

Litigation and Legal Challenges

The U.S. Chamber of Commerce announced its intention to sue over the proposed changes, accusing the CFPB of exceeding its authority.

The Chamber’s Stance

There is a fear that punctual consumers may end up subsidizing the costs of those who pay late. This contention points to a broader critique of the regulation’s fairness and balance.

Consumer Redistribution vs. Protection

The Consumer Bankers Association has also criticized the policy goals of the rule, arguing that it aims to redistribute costs among consumers rather than offer them genuine protection.

Unintended Consequences

Some see the proposed cap as a well-intentioned measure that might backfire, leading to fewer credit card offerings and a contraction in the availability of affordable credit.

These potential outcomes have sparked a debate on the best approach to protecting consumers.

Examining the $8 Fee Cap

The CFPB’s proposition sets a significantly lower threshold for late fees than current averages. By proposing a cap of $8, the bureau aims to cut down on what it sees as unnecessary and excessive charges that disproportionately affect consumers.

Potential for Higher Fees Under Certain Conditions

Despite the proposed cap, the CFPB’s “show your work” provision allows banks to charge higher fees if they can justify the costs. This element of the rule offers some flexibility but also raises questions about its practical implementation.

Industry’s Financial Concerns

The American Bankers Association has signaled that the $8 cap is substantially lower than the costs banks face when managing late payments. This discrepancy fuels the industry’s resistance and concerns over the rule’s feasibility.

A Matter of Consumer Fairness

Supporters of the cap argue that the current system disproportionately penalizes consumers for minor infractions, like late payments, with excessive fees that contribute significantly to banks’ profits at the expense of the financially vulnerable.

The Broader Economic Implications

The debate over the late fee cap touches on larger questions about consumer protection, the role of regulation in the financial industry, and the balance between corporate profitability and consumer fairness.

Legal and Regulatory Outlook

As legal challenges to the proposed rule mount, the future of the late fee cap remains uncertain. The outcome of these disputes could have lasting implications for both the regulatory environment and consumers’ wallets.

A Call for Careful Consideration

As the Biden administration moves forward with its initiative to cap credit card late fees, the financial industry’s backlash highlights the need to balance the interests of consumers and the industry.

23 Steep Taxes Adding to California Residents’ Burden

California: a place of sunshine, innovation, and, unfortunately, some of the nation’s highest taxes. From LA’s beaches to Silicon Valley’s tech hubs, residents grapple with a maze of state taxes. Here’s a glance at 23 taxes that might surprise both Californians and outsiders. 23 Steep Taxes Adding to California Residents’ Burden

Cash in on Nostalgia: 21 Toys Now Worth a Fortune

Time to dust off the boxes and find that once-cherished toy from your childhood. For collectors and enthusiasts, they items have become valued objects and they can be worth big bucks – are there any of these in your attic? Cash in on Nostalgia: 21 Toys Now Worth a Fortune

Millennials Don’t Buy These 19 Products Anymore

Millennials are changing consumer habits, quietly replacing once-staple products and traditions. Often criticized for their disruptive preferences, this generation is reshaping the marketplace with digital expertise, ethical buying, and a taste for the unconventional. Millennials Don’t Buy These 19 Products Anymore

10 Reasons Firearms Are Essential to America’s Fabric

Americans’ strong attachment to guns is influenced by constitutional rights, historical context, and cultural traditions. This article explores the cultural perspective driving their unwavering support for gun ownership, revealing the key factors shaping this enduring aspect of American life. 10 Reasons Firearms Are Essential to America’s Fabric

California’s 16 New Laws Raise Red Flags for Prospective Residents

California, celebrated for its beaches, tech prowess, and diversity, is now gaining attention for its recent legislation, prompting some residents to reconsider their residency. Explore the new laws of 2024 and the controversies and migration they’re stirring. California’s 16 New Laws Raise Red Flags for Prospective Residents

The post Biden’s Credit Card Fee Cap Sparks Financial Industry Outrage first appeared on Thrift My Life.

Featured Image Credit: Shutterstock / mark reinstein.

The content of this article is for informational purposes only and does not constitute or replace professional financial advice.