If you’re considering purchasing a home anytime soon, you may have wondered if there are any steps you can take to better position yourself for such a major financial move. The good news: there are some ways you can prepare.

How to Know if It’s the Right Time to Buy

In 2024, the housing market is expected to stabilize somewhat after a tumultuous few years.

Interest rates are starting to come down, making it a good time to look into finding your dream home.

Is the Time Right for You?

The most important question to ask yourself is whether you are financially ready to buy a home.

External factors play a part, but your own financial well-being is the biggest piece of the puzzle.

Utilize the Resources You Have

If you’re unsure, discussing your next moves with your financial advisor is always a good idea.

In the meantime, you can look at a few areas of your finances and prepare yourself for the mortgage process.

Step 1: Talk to a Professional About What You Can Afford

Speaking to a professional is one of the best things you can do to prepare for buying a home.

You might think that a real estate agent would be your first contact, but in fact, a mortgage loan officer can help you before you even start looking at homes.

What Is a Pre-Approval?

One service that a loan officer can offer you is a pre-approval, which will tell you on a surface level whether you’re currently qualified and how much you can afford to spend on a home.

Getting Pre-Approved for a Mortgage

The pre-approval process is quick, and many loan officers can provide this information to you in minutes.

It typically involves checking your credit, discussing your income and assets, and verifying that you don’t have any glaring roadblocks that could hinder your purchase plans.

Benefits of Pre-Approval

By getting pre-approved, you can start your home search with confidence that you’re shopping in the right price range.

You might find that you can afford more or less house than you thought, so the pre-approval process is crucial to helping you avoid disappointment and wasting time.

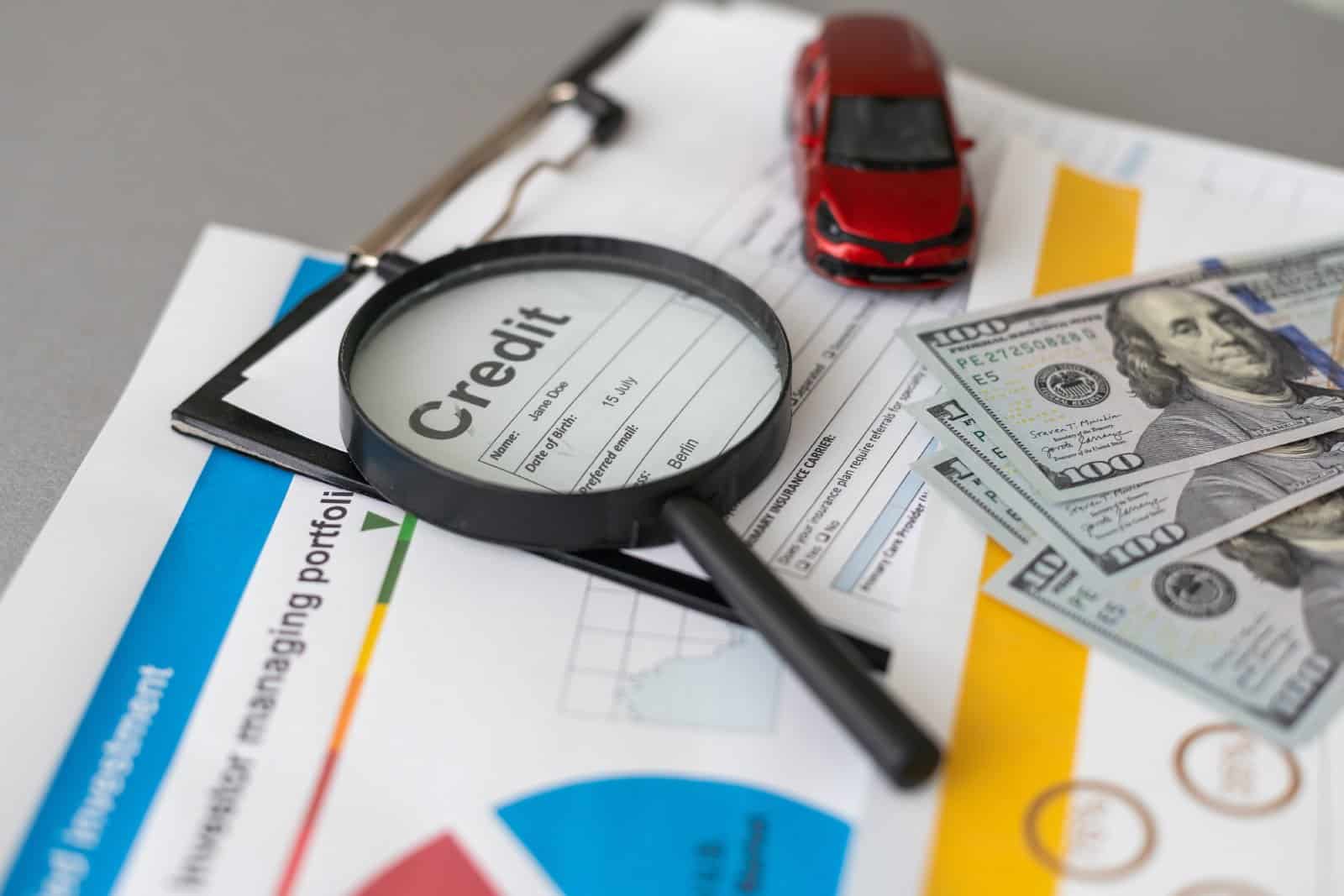

Step 2: Don’t Let Your Credit Take Any Hits

It may sound obvious, but you shouldn’t do anything that could affect your credit score while you’re preparing to buy a home until you’ve talked with your loan officer.

What Can Impact Your Score?

New loans, missing payments, or maxing out your credit cards can make a difference in your credit score. Even things like paying off large credit card balances could impact your score, so before you do something that you think will help, run it by the professionals first.

The Impact of New Debt

Financing large purchases like vehicles, furniture, or appliances can impact your score for two reasons: one; the lender will have to run your credit, prompting a credit inquiry on your report, and two; taking on new debt could mean that your debt-to-income ratio increases beyond an approvable level.

Step 3: Don’t Quit or Change Your Job

Mortgage lenders want to see that you have a steady income with a solid employment history. If you’re going to be seeking a mortgage, now is not the time to switch from a W2 job to a contract position, or take a pay cut to work in a new industry. Consistency is key!

Self-Employed Borrowers: Bring Your Paperwork

If you’re self-employed, just make sure you have good tax records and year-to-date figures to provide to your lender.

Step 4: Avoid Making Large Bank Deposits

Money is good, and the bank or mortgage lender definitely hopes to see a good savings history in your bank account! But with large deposits comes the requirement to fully source and document the funds, and the guidelines are pretty strict.

Mortgage Guidelines: Real Examples

For example, if a family member gives you a gift to help with your down payment, you’ll be required to provide documentation to show where the money came from.

Selling Big-Ticket Items

If you sell your car, the lender will require documentation to show that the new deposit on your account came from an acceptable source.

Cash is King, but Not Here

It’s a good idea to hold off on depositing large sums of cash into your account since it’s impossible to prove where the cash originated. If you do have to deposit money in order to buy your house, talk with your lender first to make sure you save the required documentation.

Step 5: Keep Thorough Records - Document Everything

On that note, it’s a good idea to assume that you’ll need documentation of just about everything you can think of. Your lender will ask for tax returns, bank statements, paystubs, and much more.

Save Your Digital Documentation

Be prepared to provide digital copies of all of your financial records. You also may be asked to write explanation letters to help the underwriter understand nuances in your financial history.

Getting Ready for the Big Move

When preparing to purchase a home, your finances will be put to the test, and having clear and transparent records of everything will help your lender get you qualified for the mortgage you need.

23 Steep Taxes Adding to California Residents’ Burden

California: a place of sunshine, innovation, and, unfortunately, some of the nation’s highest taxes. From LA’s beaches to Silicon Valley’s tech hubs, residents grapple with a maze of state taxes. Here’s a glance at 23 taxes that might surprise both Californians and outsiders. 23 Steep Taxes Adding to California Residents’ Burden

Cash in on Nostalgia: 21 Toys Now Worth a Fortune

Time to dust off the boxes and find that once-cherished toy from your childhood. For collectors and enthusiasts, these items have become valued objects, and they can be worth big bucks – are there any of these in your attic? Cash in on Nostalgia: 21 Toys Now Worth a Fortune

Millennials Don’t Buy These 19 Products Anymore

Millennials are changing consumer habits, quietly replacing once-staple products and traditions. Often criticized for their disruptive preferences, this generation is reshaping the marketplace with digital expertise, ethical buying, and a taste for the unconventional. Millennials Don’t Buy These 19 Products Anymore

The post Unlock Your Homeownership Potential with These Strategic Moves first appeared on Thrift My Life.

Featured Image Credit: Shutterstock / ChameleonsEye.

The content of this article is for informational purposes only and does not constitute or replace professional financial advice.